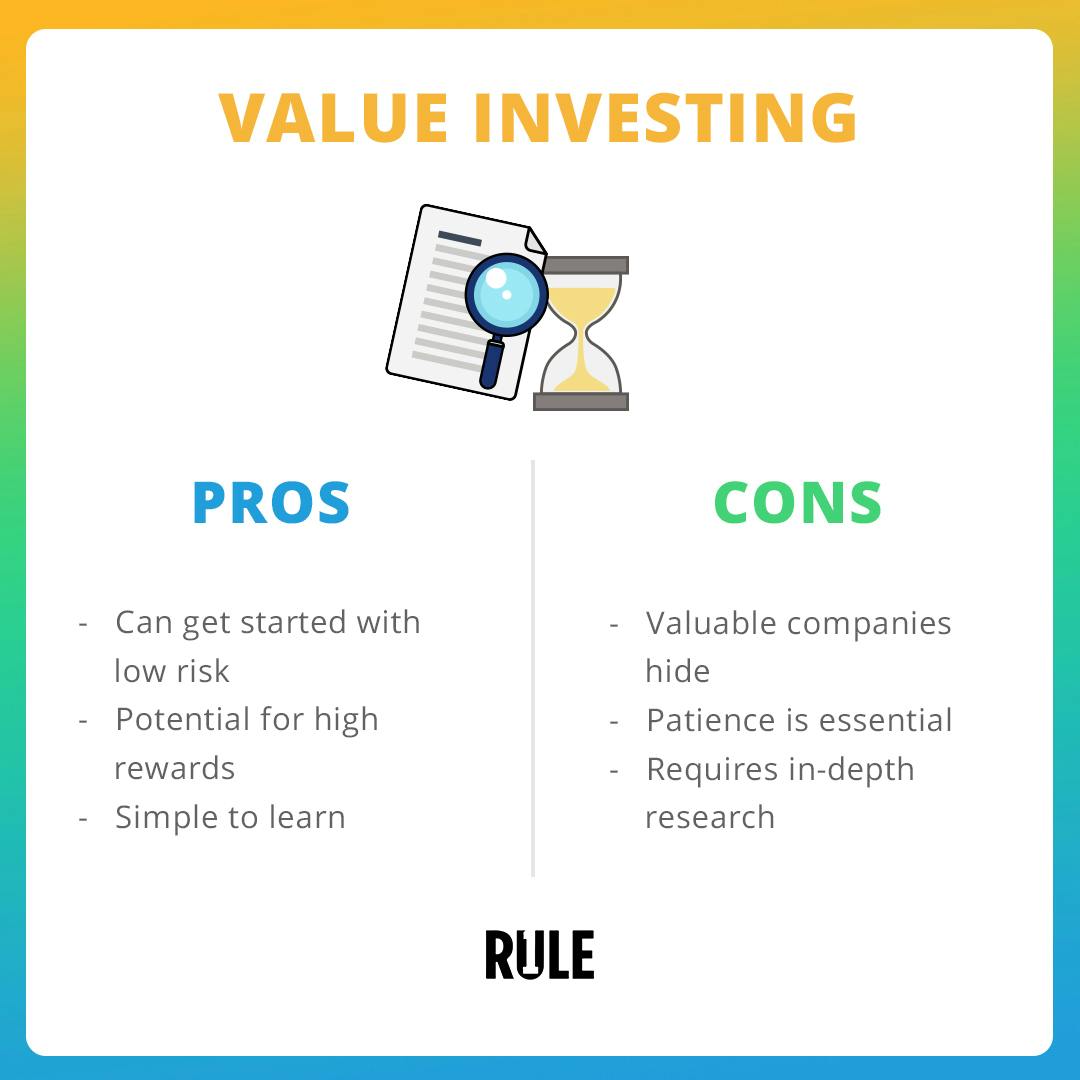

Of the many different investing strategies that a modern-day investor may choose, value investing is among the most common. It is also the foundation of the Rule One investing strategy.

Let’s dive into what value investing is and how it differs from Rule One.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.

What is Value Investing?

Value investing is a strategy focusing on buying companies with a low price-to-earnings multiple. Ben Graham, Warren Buffett’s mentor, is the father of value investing and wrote the ‘bible of value investing, ‘Security Analysis,’ in 1934. That book is still in print today.

He called this ‘value’ investing because, ideally, each investment had more value than was paid in the price. In essence, the idea is to get $10 of value for a $5 price.

Graham thought that the best way to do that was to buy quite a number of cheap companies, typically about 200, to reduce the risk that any particular business was cheap for a really good reason, like it was about to go bankrupt.

According to Graham, a company’s stock was only underpriced – and therefore worth investing in – if it could be bought for below its liquidation value. The liquidation value of a company is determined by its net assets per share.

The underlying principles of this timeless approach persist to this day, but it was particularly effective during the Great Depression and World War II, the situation in the world while Graham was investing.

The Theory Behind Value Investing

By the time Warren Buffett started investing money, though, the economy had changed, and finding deeply undervalued companies was not as easy as it had been in Graham’s time.

So what happened?

To adapt, Buffett adjusted the theory somewhat, choosing to focus on finding companies that were not only undervalued but were also wonderful businesses with a highly predictable future. This required understanding the business, a process that necessarily limited the investor to a subset of the investing universe, what Buffett called your ‘circle of competence.

The Rule One strategy draws from this evolution of the classic approach to value investing to focus on great businesses that have a few, very specific qualities.

The Rule One view of value investing dictates that the best way to make large returns on your investments is to find a few intrinsically wonderful companies run by good people and priced much lower than their actual value. A business that hits all these marks constitutes a Rule One stock.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.

What are Rule One Stocks?

At its core, a Rule One stock is a stock that is priced lower than its intrinsic value. The problem is knowing what the intrinsic value is. Intrinsic value is a term thrown around a lot regarding value investing. And that’s because it’s incredibly important.

Value investors often make decisions similar to what Ben Graham did, based on the business looking cheap, but Rule One investors know that it is better to buy a wonderful business at a fair price than a fair business at a wonderful price.

This is why Rule One investors require a deep understanding of the companies we invest in. We have to know the business well enough to know that it’s wonderful. I’ll teach you how to identify wonderful companies and determine their intrinsic value a little later on.

The Value Investing Mindset

There is a value investing mindset that is worth learning. Understanding this mindset is an important step in learning value investing. While it may not appear all that complex, buying $10 bills for $5 can be an emotional challenge, but these mindset tips will help you master it.

Fear is Your Friend

Buffett said that the secret to great investing results is to buy when there is fear.

Fear is what makes the market price of a wonderful business substantially lower than its value. In fact, fear is the only thing that makes the market price of a business wrong. Without fear around this business, industry, or economy, the business will not go on sale.

An old-school value investor decides when to buy based on a perceived low price and adjusts for the fear around this business by buying a lot of businesses so that no one business can ruin his portfolio.

But for a Rule One investor, fear is a friend because they understand the business, understand why the fear is there and have a conviction that it is irrational in the long run. Fear moves the market all the time, and if it isn’t justified, it could create excellent opportunities to buy stock in wonderful companies well below their value.

Focus on the Long-Term

Most big mutual funds are run by investors who consider themselves value investors. They talk the long game, but in fact, most big funds only hold stocks for 90 days or less. Rule One investors are actually long-term investors.

For example, I held one stock for 40 years. Rule One strategy is not a get-rich-quick scheme; it’s a buy-and-hold strategy. Once you find a company priced lower than its actual value, if it’s wonderful, you’ll want to hold it forever.

When operating as a Rule One investor, you need to be patient and keep your focus on long-term profits.

Do Your Research

Many value investors almost pick stocks at random. If the PE is low, it’s on the buy list.

Rule One investors know they have to thoroughly analyze the business just to figure out its worth and value investment potential.

True value investments require a lot of research. To have a deep understanding of the companies you are investing in, you have to understand the business: how they operate, the pros and cons of their industry, their management, their financials, and more. But the more you know, the better decisions you’ll make and the better returns you’ll get.

Wait For the Right Time To Buy

When you analyze a company thoroughly, you may discover that it would make a wonderful investment, but the market does not underprice it… that doesn’t mean it won’t become underpriced at some point.

A key component of good solid Rule One investing is buying businesses at the right time and having the mindset that the right time will present itself if you’re patient.

Everyday stock market volatility and events such as recessions, market crashes, negative publicity, among others, create opportunities for value investors to jump in and buy when the price drops.

How To Identify Underpriced Companies

Learning how to identify underpriced companies is central to value investing.

But here’s the kicker: This skill takes a good deal of training; the market doesn’t underprice companies every day, and it almost always makes it look very scary when it does.

Finding underpriced companies every day is not going to happen. Or, if it does, you’re doing it wrong. This is why many people don’t take advantage of the value investing strategy. It requires a lot of patience. Charlie Munger said we don’t make money when we buy, and we don’t make money when we sell; we make money when we wait.

Use The 4-Ms

In addition to spotting undervalued companies, it’s also important to ensure that the companies you are investing in are high-quality enough to retain their value throughout the time you are holding them. I like to evaluate whether a business is a wonderful company with what I call the 4-Ms of Investing: Meaning, Management, Moat, and Margin of Safety.

If you can check off each of these 4-Ms for a company you are considering investing in, it will be well worth your while.

Meaning

You must understand the meaning of the business.

How does this industry work, who are the competitors, and how do they compete? And how does this business fit your personal values? Does it have meaning to you personally? This is important because if it has meaning to you, you’ll better understand what it does and how it works and will be more likely to do the research necessary to understand all elements of the business that affect its value.

Management

The company needs to have management that is talented and has integrity. Perform a background check on the leaders in charge of guiding the company, paying close attention to their honesty, transparency, and success of their prior positions to determine if they are good, solid leaders that will take the company in the right direction. And, super critical, do they allocate capital well?

Moat

The company should have a moat. A moat is something intrinsic to the business, making it very difficult for competitors to compete. If a company has patented technology, a network of users, control over the market, an impenetrable brand, or a product or service customers would never switch from; it has a moat.

Margin of Safety

To guarantee good returns, you must buy a company at a price that gives you a margin of safety. For Rule One investors, 50% off of the value is the margin of safety to look for. This provides a buffer that makes it possible to still experience gains even if problems arise. This is the final M, but arguably the most important.

These 4-Ms separate Rule One investing from value investing. Both sets of rules dictate that you must buy a company cheaply, but Rule One strategy requires a much deeper understanding of the business because we’re not going to offset risk by buying 200 businesses. We reduce risk with knowledge. That’s the bottom line.

What's your Investing IQ?

See how you stack up against other investors.Use Investment Calculators

As an investor living in the digital age, you have a lot of advantages that investors who came before you did not.

One of those advantages is access to software-based tools designed to help you determine a company’s investment potential.

On the Rule One website, we offer a number of free investment calculators to help you learn to crunch important investment numbers along your way.

If you need a little extra help determining whether or not a company is priced well below its value and is a good value investment, checking out these free tools is a great place to start.

Common Questions About Rule One Investing

You may have questions about our view of value investing, as any intelligent investor would. I’ve answered a few of the most common questions about this strategy here to help you decide if it is right for you.

Can Rule One Investing Make You Rich?

When Warren Buffett first started investing, he used the Rule One value investing principles to quickly grow a small initial investment into a large fortune. In fact, he coined the term ‘Rule One.’ He said there are only two rules of investing. Rule #1 – don’t lose money, and Rule #2 – don’t forget Rule #1.

In short, it is certainly safe to say that the strategy can make you a lot of money.

In fact, to this day, many of the world’s most successful investors could be classified as Rule One investors in some form or another.

Are the Returns on Rule One Stocks Usually Good?

Typically, great returns from Rule One investing happen whenever the market realizes that a company is undervalued and raises its stock price back to its real value. This is one of the foundational principles of Rule One investing: markets eventually correct underpriced stocks to their intrinsic values.

So, investors who invest in great businesses when priced at 50% of their intrinsic value can stand to make a 100% return on their investment when the market ultimately corrects.

This may very well take some time (remember, value investing is a long-term strategy). It can even take several years from the time you purchase stock in a company you deem to be underpriced to the time it reaches its true value, but when it does, you can experience incredible returns. If it takes three years, your annual compounded return for all three years is 26% per year.

So, if you do manage to find a company that is truly underpriced, the underlying logic dictates that the returns will come in time.

Bottom line: Rule One investing is long-term investing, but patience will pay off.

How Does Rule One Investing Compare to Other Investment Strategies?

Comparing and contrasting the advantages and disadvantages of Rule One investing with other investment strategies can help you better understand what exactly it is and what it is not.

Some of the most popular investment strategies out there today include day trading, index investing and growth investing. Let’s discuss the key differences between these strategies and Rule One investing.

Day Trading vs. Rule One Investing

Day trading has become a trendy option with investors because the big wins are publicized (not the big losses). The most significant difference between Rule One investing and day trading is that the first focuses on the long term while the latter focuses on the very short term.

Day trading is also a lot more like gambling—betting on short-term fluctuations with high risk, whereas value investing focuses on minimizing risk by maximizing knowledge.

Index Investing vs. Rule One Investing

Investing in index funds is a popular option because it is arguably the most hands-off form of investing and requires very little research. However, it’s also speculative because you simply put your money in an index fund that tracks hundreds of companies traded on the stock market, cross your fingers, and hope that the market goes up.

With Rule One investing, you choose individual companies and buy them at discounted prices. When you buy $10 of value for $5, you are certain to make money; you just don’t know exactly when.

Growth Investing vs. Rule One Investing

Growth investing is the practice of investing in rapidly growing companies with high PE ratios; thus, growth investing is the polar opposite of value investing. That isn’t true of Rule One investing. Rule One investors buy value companies and growth companies.

In reality, what are typically considered “growth stocks” can also be “value stocks,” and you can invest in them as part of your Rule One investing strategy. We don’t care about how quickly or slowly a company is growing. What we care about is that we are getting $10 of value for $5.

Value Investing Resources

As already mentioned, learning how to identify companies that the market has put on sale takes a little bit of knowledge and training.

Thankfully, there is no shortage of resources available that you can use to learn all about value investing strategies and principles.

Value Investing Books

A book on value investing is a great place to start.

A few of my favorites include:

The Intelligent Investor by Ben Graham

Poor Charlie’s Almanack: The Wit and Wisdom of Charles T. Munger by Peter D. Kaufman

The Essays of Warren Buffett by Lawrence Cunningham

The Dhandho Investor by Mohnish Pabrai

Security Analysis by Ben Graham and David Dodd

I have also published 3 New York Times Best-Selling Books based on the principles of value investing seen through the lens of Rule #1.

If you’re looking for a book that will take you from knowing next to nothing about investing to becoming a successful investor in little time at all, these are great books to consider checking out.

Rule One Investing Podcast

Podcasts are another great, easily accessible, and digestible way to learn the art of value investing. Each week, my daughter and I host a Rule One investing podcast called InvestED.

If you are looking for a way to learn all about key investing strategies while you’re in the car, working around the house, or at the gym, queuing up with this podcast is a great option to consider.

Rule One Investing Workshop

If you prefer a more hands-on approach to learning, then my Investing Workshop may be right for you.

This transformational workshop is designed to teach you everything you need to know to get started as a Rule One investor in an enjoyable environment where you can ask questions and learn from the like-minded people around you.

Rule One Investing Webinar

For another virtual option, consider my free Investing Webinar.

In this webinar, I go over some of the basic strategies used by the most successful investors in the world today. These strategies draw heavily from the concept of value investing, making this Rule One webinar a great way to get started learning to invest.

On the surface, Rule One investing is simple; it entails buying companies priced lower than their actual value. However, knowing what you’re buying can be a real challenge.

With these tips and tools, you can learn this proven investing strategy and become a more successful value investor.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.