Unveiling the Power of Growth Rates in Business Analysis

By understanding growth rates, investors can make more informed decisions and discover the hidden gems of the business world. Let's dive deep into the process of determining growth rates, where to find these essential numbers, and how to avoid over-analysis.

Deciphering the Power of Growth Rates

Imagine you're presented with two businesses, both with different rates of growth. The growth rate of a business is a critical factor in valuing it. A company that can sustain a growth rate of 15 percent annually holds a higher valuation than one growing at a mere 5 percent. This reflects the future value that investors assign to a business's current earnings. Additionally, higher growth rates often indicate the presence of a strong competitive advantage or "moat," making earnings growth more certain.

The Big Five: Sales, EPS, Equity, and Cash Growth Rates

The growth rates of Sales, Earnings Per Share (EPS), Equity, and Cash are the key players in determining a company's potential. These growth rates provide insights into the company's financial health, its ability to generate returns, and its growth trajectory.

Unveiling Growth Rates: A Detailed Look

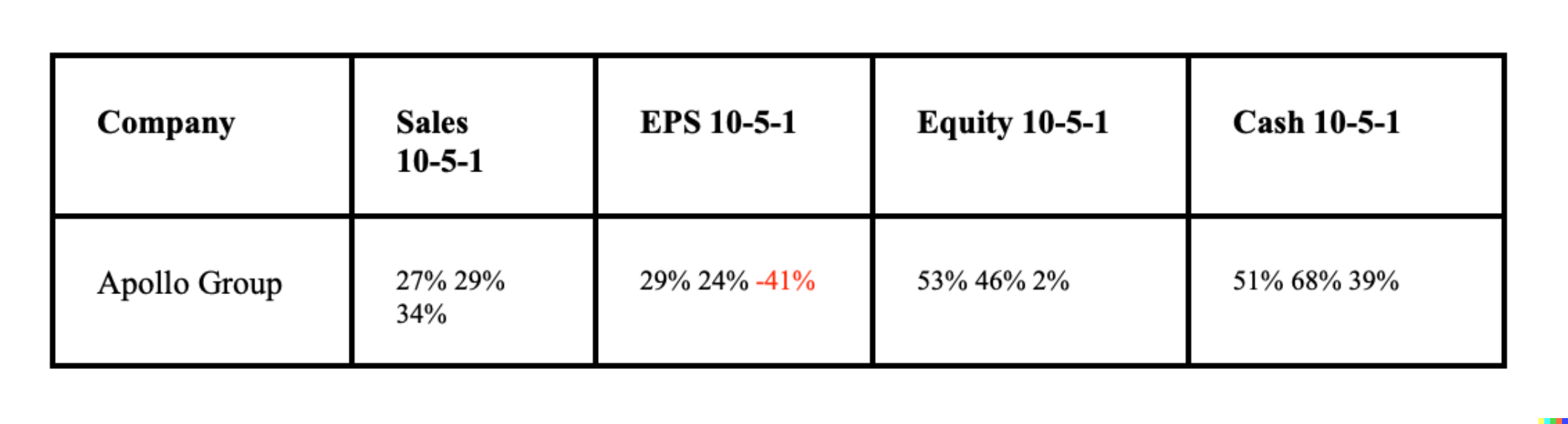

To grasp the significance of growth rates, let's analyze the growth rates of Apollo Group as an example. By examining the 10-year, 5-year, and 1-year growth rates for Sales, EPS, Equity, and Cash, we can gain insights into the company's performance and potential problems.

Interpreting Growth Rates: Apollo Group vs. ITT Educational

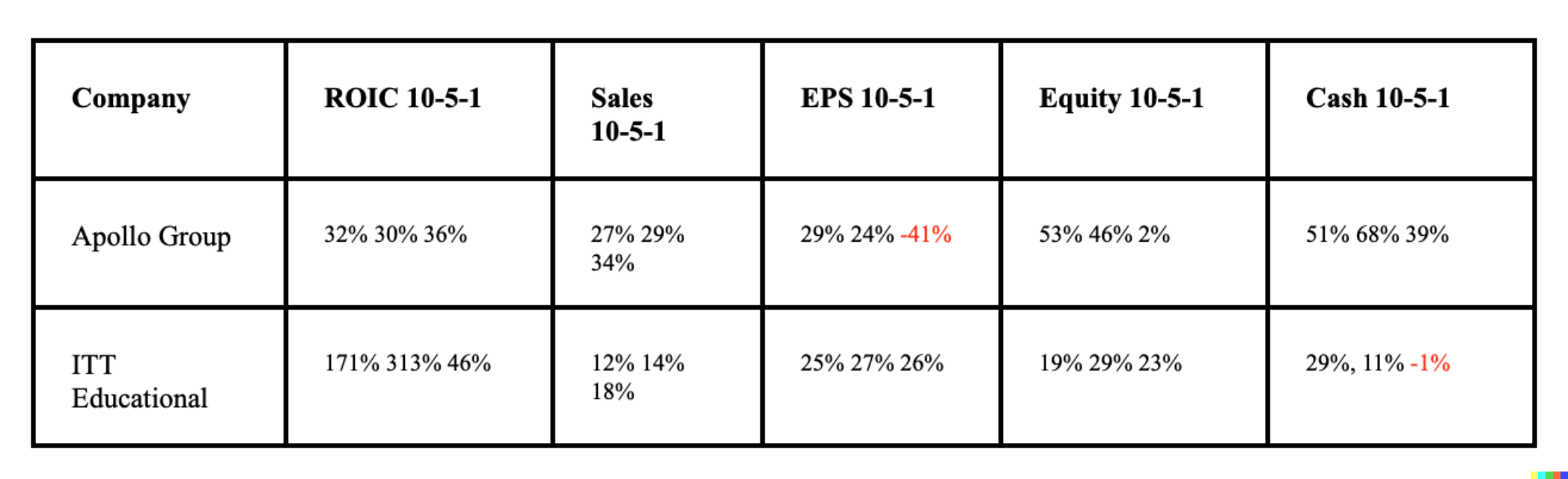

Comparing growth rates between companies sheds light on their competitive strengths. Let's compare Apollo Group with ITT Educational using their growth rates for ROIC, Sales, EPS, Equity, and Cash. While both companies boast impressive ROIC and Sales growth rates, a closer look at the other growth rates reveals the dynamics of their businesses.

Unveiling the Big Five Numbers: Where to Find Them

Invest wisely, gathering information and making informed decisions.

The good news is that you don't need to be a financial wizard to access these growth rate numbers. We've compiled that data for you in the Rule #1 Toolbox. There are some tutorial videos in the toolbox to help you get more acquainted with the tool and its many functions.

Avoid Over-Analysis: Focus on the Key Numbers

Over-analysis can lead to paralysis, and simplicity is often the key. Focusing on the key numbers, like Sales, Earnings, Equity, and Cash, allows you to swiftly evaluate a business's potential. These essential figures are available on various financial sites and presented in a similar format, which makes the process of extracting vital information straightforward.

The Road Ahead: Empowering Yourself with Growth Rates

Understanding growth rates gives you a powerful tool to evaluate businesses and make investment decisions. By mastering the art of deciphering these rates, you can uncover valuable opportunities and make informed choices that align with your investment goals. So, let's embark on this journey of growth rates and empower ourselves with the knowledge to navigate the world of investments with confidence!