You know the things we consistently put off because we don’t want to think about them? Or because we believe we can circle back to them later?

Retirement is one of those things.

But, I’m here to tell you it shouldn’t be. In reality, retirement is a lot closer than you might realize, so it’s important to start planning now to ensure you’re able to build a comfortable, sustainable life that exists outside of a regular paycheck.

Though there are many ways to plan for retirement, there is only one that will best suit your lifestyle. Before you dive into any investment options or strategies, take a few minutes to ask yourself some key questions about how you want to spend your days outside of the corporate world, like:

What type of lifestyle do you want to live?

What activities would you like to participate in?

How much will these things cost you?

How much progress have you made in pursuit of the ideal amount of money you hope to retire with?

After considering these questions, then you can begin thinking about which type of qualified retirement plan is right for you. To get the conversation started, let’s compare two popular plan options: a pension vs. 401k.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.

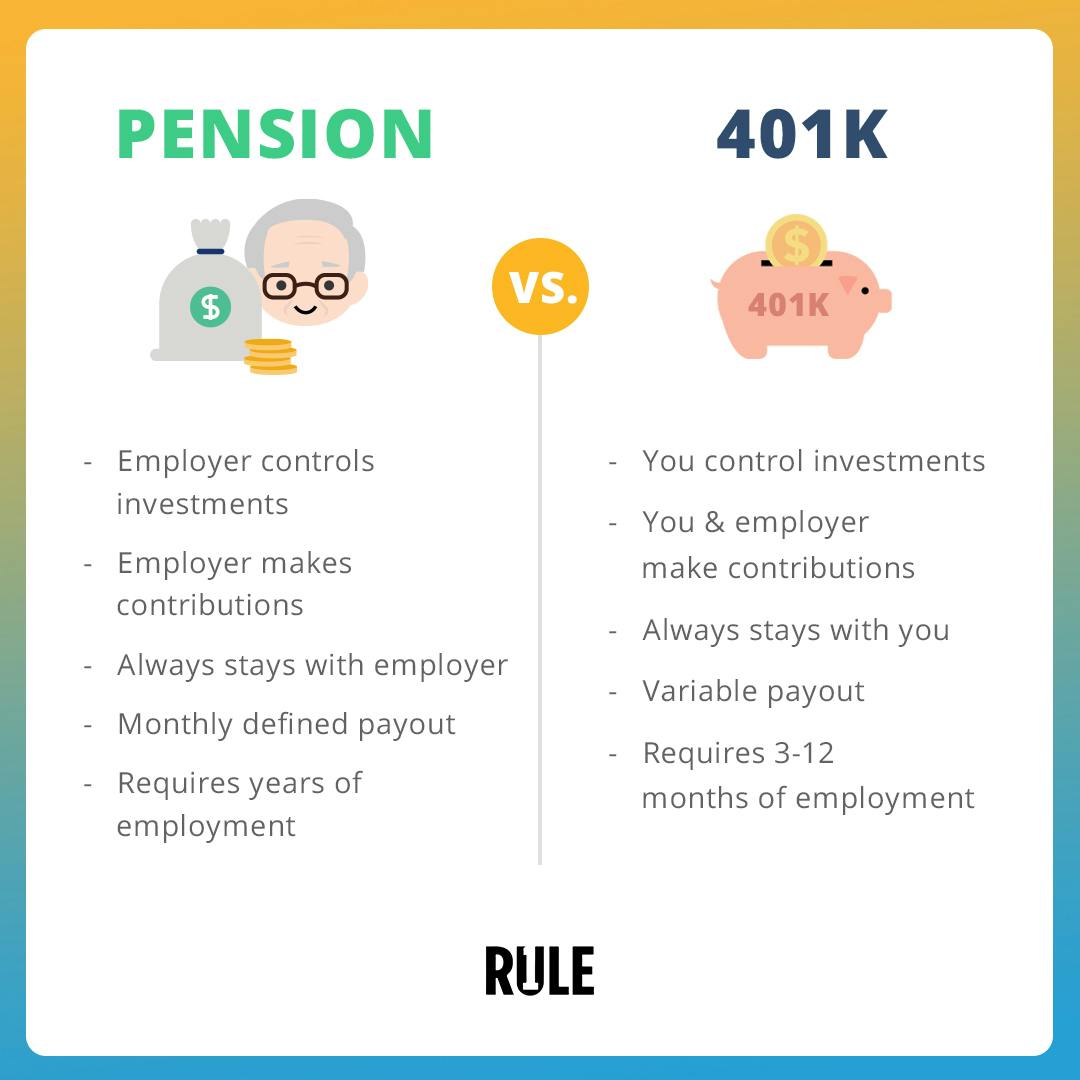

Pension vs. 401k: What’s the Difference?

Pensions and 401ks are both types of employer-sponsored retirement plans that are cut from the same cloth. However, the most noteworthy difference between a pension and a 401k is that a 401k is a defined-contribution plan, whereas a pension is a defined-benefit plan.

Let’s dig into each of these a little more.

What is a Pension?

A pension is a qualified retirement plan that provides workers with a set amount of money per month in retirement, provided they meet specific criteria.

This allocation could be set or based on a formula that factors in your annual salary and how many years you held a certain role within your company.

When you plan on retiring with a pension, your employer agrees to take on all income risks once you’re done working, which means your account will be unaffected by any fluctuations that occur within the market.

Pension Plans

Cash balance plans, such as pension plans, are typically overseen by the company offering the benefits, but they all share a common structure. As mentioned, many employers will require employees to work for a set number of years before they are eligible for a pension plan.

Once you choose a pension plan, you must be okay with foregoing the ability to make any investment decisions. Contributions will be made to your investment portfolio by your employer and they will be managed separately by an experienced investment professional. Plus, it’s important to note that you will continue to earn the same amount regardless of how your pension’s investments fare.

Depending on the type of pension plan you have, you may also have the opportunity to allocate a portion of your benefits to a spouse or beneficiary after you die.

What is a 401k?

A 401k is a qualified retirement plan that allows both employees and employers to contribute and invest funds that can be used for retirement. In many cases, companies will match a specific percentage of the money that you are putting away for the future.

Through this type of retirement plan, individuals work with a 401k provider to contribute money into various investment buckets, which include mutual funds in the form of stocks, bonds, securities, or annuities. Due to the nature of this type of plan, it is crucial to monitor changes in the market so you can protect your 401k from a stock market crash if necessary.

Investments that are contributed to a 401k account are tax-free and there is no growth limit for an individual account. However, there is a cap on the annual amount you can contribute.

401k Plans

When you sign up for a 401k retirement plan, the percentage of funds you decide to contribute will be automatically deducted from each paycheck you receive from your employer.

There are two types of 401k plans—each with different tax implications—and the one you choose will depend on your current financial situation and which options are available through your 401k provider.

If you choose a Traditional 401k, the money you contribute to your account will be excluded from your taxable income. This means that this investment will grow tax-deferred, but when you withdraw the money in retirement, you will be responsible for paying taxes on the accrued amount.

This is not the case with a Roth 401k. A Roth plan allows you to contribute money that you’ve already paid taxes on, that will still grow tax-deferred. In this scenario, you will be able to make tax-free withdrawals once you’ve left the workforce.

Pension vs 401k: Which is Better?

When it comes to identifying a qualified retirement plan that works for you, determining whether a pension vs 401k would be a better fit depends on a variety of individual factors.

Pensions can be the safest all-around investment since risks will be managed by your employer and you will be guaranteed that set income for the remainder of your life.

Even still, solely retiring with a pension is one of many money traps to avoid in your later years. Social Security benefits are not what they once were, so you most likely won’t be unable to afford your current lifestyle in retirement if this is your only strategy.

Which Has Better ROI?

If you’re wondering whether to invest in your company’s 401k instead, there is some return on investment differences between a pension and 401k.

As I mentioned, a 401k will put you directly in charge of your investments, their growth, and the money you will be able to save for later.

Retiring with a 401k also offers more flexibility than retiring with a pension since the funds can be moved if you decide to change jobs or open up an IRA account. Transferring funds from one 401k provider to another is a fairly simple process.

A pension, on the other hand, cannot be moved. It’s always in the hands of the employer that manages it. Due to this limited flexibility, many companies have stopped offering pensions, and instead, promote the slew of benefits associated with a 401k.

At Rule #1 investors, we prefer 401ks over cash balance plans because they put you in the driver’s seat and allow you to move your investments in a positive direction.

Tips for Investing After Retirement

Your money management knowledge shouldn’t just evaporate because you’re no longer working. Once you’re able to enjoy your regularly scheduled time away from the office, you’ll want to make the most out of the money you’ve saved.

And if you didn’t quite hit your goal number by the time you finished working, beginning to invest can help you bridge the gap between your current financial situation and your aspirations.

If you decide to start investing after you retire, you’ll want to eliminate bad, high-interest debt first. The longer this debt lingers, the more it will hold you back from the financial future you desire.

Second, you’ll want to embrace the mentality of starting small. This may sound counterproductive, but if you familiarize yourself with businesses that you have a lot of knowledge about, you’ll be able to make smarter investment decisions.

If there are stocks in the market that you already know about and expert investors are interested in, you can walk away confidently knowing that your investments are earning you the ROI you need to bolster your long-term wealth.

And last but not least, you’ll want to focus on staying within a cash environment and wait for one of the companies that you have your eye on to go on sale, which typically happens when the stock market crashes. One of these cycles presents the perfect low-risk opportunity for buying wonderful companies at a discounted price that will double their return within just a few years.

And, all of this is possible while in retirement.

Start Planning Your Retirement Today

So, if you want to know exactly how to start investing or need a refresher on the best strategies for success, become a Rule #1 investor. Our resources go beyond explaining the difference between a pension vs 401k. We provide you with actionable insights that you can use to start investing like some of the best in the business.

But, wait. Weren’t we just talking about retirement?

It’s getting more and more difficult to retire on your timeline, and most people won’t even save enough money to make it last through their retirement.

So, if you want to examine your current financial situation to figure out whether a pension vs. 401k is right for you, take my Retirement Quiz. It includes a short list of questions that will give you real insights into how prepared you are for life after work.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.