A bunch of you have written in about Claire's jewelry store (CLE), so here's a homework for you, from Meg.

Dear Phil Town,

First off, geez this is fun! I've enjoyed trying to find wonderful companies so much, my husband has taken to calling it my version of Internet porn – addictive. ;-)

Here's my homework for your perusal:

Meaning – My eight-year-old thinks it is the coolest store EVER. She managed to make a $20 gift card to Claire's last over a hour of browsing their wares, and the salespeople are always nice to their pint-size diva-in-training customers. Plus, their knack for catering to this customer has been around longer than I care to admit; I got my ears pierced at Claire's on the 13th birthday.

Moat – Brand, baby – practically every mall everywhere, including a growing international base.

Management – This is such a great American success story – two sisters as co-CEOs who grew-up working at Claire's. Both their ailing father, the founder, and the BOD thought they were not up for the task. Well, four years later, and the business has never been bigger, better, and well managed. You go girls!

My Big 5 Numbers (using freebie information on MSN) – ROIC, Equity, EPS, and Cash all are well above the required 10% and growing nicely, plus, no long-term debt. Now I may have failed my homework because the Sales percent is a wee-bit low on 3 out of the 9 years. I need to work on my ability to see only in black and white.

MOS:

Using an estimated future EPS growth rate of 15.5% and an estimated future PE of 31% the MOS price is $56.33. And wahoo, today's closing stock price was $25.47. What a bargain! The final icing on the cake is that the three tools look as though it will be time to buy soon.

So, is all this excitement for naught due the sales percentages not being 100% perfect?

Thanks Phil for providing me an amazing opportunity to revamp my family's financial future.

Warm regards,

Meg

Phil's response:

Hi Meg,

Nice find! The Big Five numbers look pretty wonderful, actually. ROIC in particular is just off the chart. Love that. It tells us that the CEO sisters are all about watching to make sure the rate of return on surplus capital stays high. They get a big kiss.

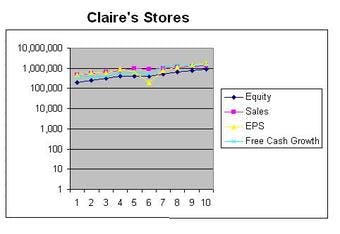

I am including this chart that shows (on a log scale) the history of the big four growth rates.

You can see that they hit a bump a few years ago, but all in all this is a very consistent business model these ladies are running.

That said, Meg, you did point out that the Sales numbers are below the required 10% for the last year and last 5 years.

Investools is giving us a wrong number here, I think. They show 8%. I get 9%. 9 is a whole lot closer to the mark than 8 so I'm going to leave it to you to cut these ladies some slack here if you want to.

Clearly their sales growth numbers are sliding slowly while everything else is rolling along at a very healthy 16% clip. What does that tell you about the business?

Didn't you mention that Claire's is in 'every' shopping mall? Which leads us to this point:

The present Sticker price of a business is determined by the future surplus cash / earnings that the business will produce into the future. Note that the value of a business is not determined by its sales... but by the cash -- which shows up as EPS growth, Equity growth and Free Cash Growth.

If we're going to have one sub par number for a business like Claire's, let's have it be sales growth. Still, we have to estimate based on the fact that they are everywhere that growth must inevitably slow.

Your mission, should you decide to accept it, is to defend the growth rate you are putting in there. Can Claire's really continue to grow its surplus at 15%? Perhaps it can, but I'd want to hear it from the CEOs. Have you listened in on their quarterly calls? Go to the Investor Relations part of Claire's website and dig around.

And here's the most worrisome part of the MOS: You are using a 30 PE. And that's fine from both a historical and Rule #1 perspective since the PE over the last 5 years has ranged from 8 to 50.

But when you look at PE more closely you might see that the PE is quite a lot lower lately. More like a high of 20 or so. And it hasn't seen a 50 PE since way back when its earnings were horrible.

I kind of wonder if you've got to drop that PE a bit to conform more with their best upside PE lately. Using a 20 I get Sticker of $35 and a MOS of $18. Using a 25 PE I get a Sticker of $44 and a MOS of $22. It's selling for $25.

You have to tell me whether the 25 PE is justified for the future. But even with a 20, if you really like this it still has barely enough MOS to get in if you really really understand the biz.

Now go play!