George had asked this question about CHS recently:

i love the book; it's got the ring of truth, but i'm new and still waiting 'till i feel confident! i read the blog about CHS & when i ran the rule #1 numbers a question arose:

the 9 year equity (BVPS) rate from 1997-2006, goes 48%, 53%, 53%, 53%, 52%, 50%, 47%, 44%, 42%.

the last years you can see the growth rate descending, but the rate is so very high above the the 10% minimum for which we are looking, i just have to ask:

does this high rate every year override the principle that the growth need to be climbing each year?

thanks,george

This is a good question. You see a business that has Meaning to you in the Rule #1 sense of the word and you want to determine the future growth rate. You do the Big Five Numbers and see that the growth rate is consistent across all numbers and it's very high. But it's also declining a bit every year.

First, is this a bad sign, and second, how do we estimate the future growth rate if the historical rates are sliding every year?

A really high rate of growth usually only happens when a business is relatively new and has something unique. You see it a lot in high tech companies and in some kinds of retail.

If the rate of growth is coming down, it isn't necessarily a sign of a problem with the Moat. It's just a mathematical issue. The bigger a business gets, the harder it is to sustain any given growth rate because every year the bar got raised that you not only have to beat, but exceed by the same percentage you exceeded it the year before.

Obviously at some point that gets to be impossible if your original growth rate was very high -- if only because the power of compounding high sustained growth results in a business being too big for its entire market.

This was the problem with forecasting continued high growth for Yahoo in 1999. For Yahoo to sustain the growth rate necessary to justify its $135 price tag it would have to quickly become the largest business in the world. Which seemed unlikely for a website portal business.

So the law of projections is that if a trend can't be sustained, it will stop.

It stopped and Yahoo is now selling for $28. (Of course it didn't help Yahoo that Google came out of nowhere and is kicking its butt -- but that's the nature of technology and the reason that it is risky to project into the ten year future for a high tech business, and the reason Google stays in the Risky Biz portfolio.)

Point being that extremely high growth rates are great but not sustainable. Therefore we have to use a lower rate for a ten year projection. But WHAT rate?

One way to decide is to look at what growth rate really successful businesses in that or similar industries have been able to sustain for long periods of time and use that rate.

For example, some retail businesses have been able to sustain growth rates of 15% for over twenty years. Walgreens, for example, grew its stock price from $0.05 to $44 over 30 years. Over 9 doubles. Call it 3 years to double once. That's about 24% for 30 years for price growth.

Obviously they were way undervalued in 1975 but they fueled that incredible price growth with a sustained 15% growth rate in sales, earnings, book value and cash with amazingly high consistency. (Today, by the way, WAG is worth about $56 and selling for $40. Gotta love that, sports fans. If you've been keeping up on WAG and been a buyer, you are looking at buying back in at anything under $44.)

Urban Outfitters, a trendy clothing store chain, has been on a nice run for many years well in excess of 20% across the board with incredible consistency.

The key to look for once you've checked out the potential for long term growth is to see consistency across all the growth numbers and a rock solid ROIC number.

Forget EPS all by itself. You don't want to use a number that is vastly higher than what cash, sales and the all-important book value are growing at. In fact, I point out in Rule #1 that if I had to use just one number to determine the future growth rate, I'd use the Book Value Per Share growth rate. It is, after all, the number that grows because of surplus cash, and that is the best indicator of a healthy Moat.

But the MOST critical thing to see is that the numbers are consistent across all the key numbers. That's what lets us be so arrogant as to assume we can actually figure out what this business is worth.

I'd say most businesses are pretty much impossible to put a really good long term value on. You can always find the liquidation value, but that's hardly the real value of a business, is it? We want to know what this thing is worth as a going concern that produces surplus cash. But most businesses either have no moat and are, therefore, subject to possible sudden destruction, or are too inconsistent to really know what they are going to grow like in the future.

We're stuck with finding those few that we think we really can put a value on and sticking to those.

So let's look at Chico's through that Rule #1 lens.

Chico's numbers are incredible, but the concern is that the EPS numbers are sliding down from 60% average over the last ten years to a TTM year over year of 22% -- and there may be more slowing in the near term.

The analysts' expectations for the next five years range from 15% to 30% and average 22%. So that's one number.

What we're really looking for is whether we're going to come up with a lower number than that for CHS.

If we get a higher number on our own, we're going to use the analysts' number simply because its more conservative. Yes, sports fans, when you get better at this, you, too, can use your number if it's higher than the analysts', but don't do that until you are investing for at least five years successfully.

Until then, be patient, be conservative and don't violate Rule #1.

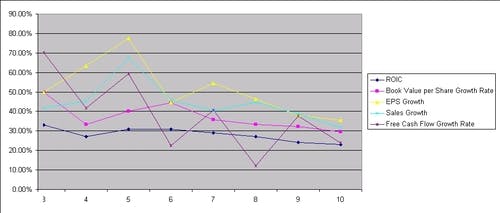

CHS's BVPS growth rate is consistently at or above 30% right up to now.

Sales are sliding some from 37% to 32% and Free Cash is ranging down from 29% to 23%.

So based on historical numbers, we're not likely to be lower than the analysts' 22%. The only thing that would bring us to a lower number to use for future growth is if we think something is off that isn't showing up in the numbers.

That something might be the CEO telling us that the business is going to grow at about 15% a year.

CEOs do that from time to time. Meg Whitman at Ebay did it a couple of years ago. Michael Dell at DELL did it last year. John Mackey at Whole Foods did it a couple of weeks ago.

Some analysts simply dismiss what the CEO says, but I'm going to listen for the simple reason that I wouldn't be investing with this CEO if I didn't think he or she was the kind of CEO who tells investors the truth. I don't expect my CEO to sandbag me or hype the future. I expect them to give me the information that I need to determine the value of this business. If they give it to me and I don't believe it, then why am I investing in this business in the first place? (Hopefully you start to see how integrated the 4M analysis really is.)

There is one more key number to discuss: ROIC.

Return on Invested Capital tells us that the CEO is managing the business well. As long as that number isn't dropping from where it was long term, things are going pretty darn good in terms of how the capital is being invested. The CEO is putting money in places that are producing solid historical returns.

CHS's ROIC is hanging right at the same high level that it was ten years ago: 23%. Awesome.

Short of the CEO telling me something that puts the growth rate lower than the average analyst, in this case, I'm going to go with 22%. It's below all the long term growth rates of the business. And best of all, its a doable number if the business keeps on being really great.

In CHS's case, that is the question. They've got issues. They lost a key person. The red flags are up. So dig in there and see if you KNOW that this is a great business for the future.

Are you sure that CHS will be a player in women's fashion stores twenty years from now... the way I'm sure that Harley Davidson will be a force in motorcycles in twenty years? You better be. It's your money. But if you love it that much, then I'd value it with 22%.

With a PE that ranges from 13 to 60, we've got good reason to believe that using a 44 (2 x the 22% growth rate) isn't out of the question, and that happens to be both the Rule #1 PE and the historical PE.

(Which is a nice not-so-coincidental result. If you are getting growth rates that consistently result in a much higher PE than the historical PE, something might be amiss in your view of the predictablility of the business.) In this case, we gotta be kind of happy with the result.

And the $86 Sticker Price gives us an MOS of $43.

And the price when I wrote this is... ta da... $23.

Should be interesting for you women's clothing folks. Think the Big Guys got scared for all the right reasons that can make us a pile of money? Makes me want to learn the business, seeing a price that far below a reasonable Sticker. I just might have to get into it. See if I can figure out if Chico's will be around in twenty.

Or is Coldwater Creek a better business to own? Or do I want to be trendy and own Urban or another business in this industry?

And that's how it goes for us Rule #1 types. You see something this cheap and you want to dig in and find out if it really is a great long term business, and off you go learning something. Darn, I hate it when that happens. Totally interferes with my snowboarding.

Now go play.

Phil

P.S. As an addendum:

I built this chart of CHS in Excel by pasting the growth rates from Investools into Excel and hitting the chart button. Simple, but it shows us the trend doesn't it?

You can see that 22% growth rate is right where we want to be if we believe that this thing is going to level off at a sustainable rate. But what happens if it continues on down to the bottom of the analyst range of estimates -- 15%?

That growth rate lowers out PE to 30 and the Sticker to $34. Puts the MOS at $17. With the price at $23, even with some pretty conservative projections, the biz is still buyable for all you expert CHS owners out there.