When we talk about financial investments, a few of the most important things to keep in mind are where you're going to house your money and the choices that follow about how you'll go about investing it.

Many investment vehicles can help investors like you build wealth. In my NY Times #1 best seller, Payback Time, I called these vehicles' Berkies' in a nod to Berkshire Hathaway. Berkshire is Buffett's vehicle, but not all of us can create a corporation to invest through.

In fact, it's not even recommended, and once, Charlie Munger said it was a really dumb idea that just sort of worked out. That said, let's take a look at what these investment vehicles are.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.

What Are Investment Vehicles?

An investment vehicle describes the legal container into which you place and manage your money. Control, fee structures, costs, and benefits can vary based on your chosen investment vehicle.

Ideally, we should all choose investment vehicles that will allow us to invest freely in any business we'd like without being taxed on the gains. Ever. Let's examine why this is.

WHY TAXATION MATTERS

Taxation matters. It really does.

If you could simply buy stocks and hold them, taxes would not be a concern. However, there are specific times when it's beneficial to sell to ensure your investments maximize the compounded annual growth rate of your capital.

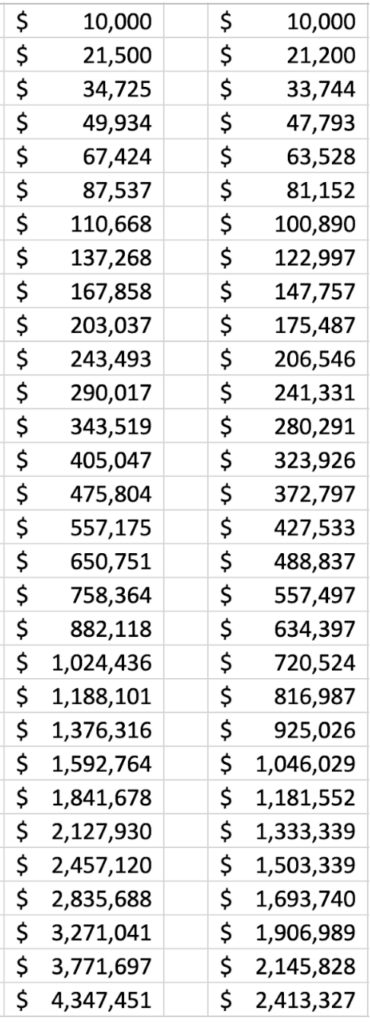

Here is a chart that shows the impact of taxation on compounding rates of return.

The first column starts with $10,000, adds $10,000 per year, and grows the money at 15% per year, compounded for 30 years, without taxation.

The second column does the same thing but also assumes you are taxed yearly on your 15% annual gains at the normal long-term capital gains tax rate of 20%.

Mathematically, that means the government reduced your compounded rate of return from 15% to 12%. That doesn't seem like much but what it does is horrible. It means that government taxation chopped your retirement capital in half. Hard to believe, I know, but here is the data:

ROTH IRA

Only one kind of vehicle lets you off the hook for taxation and can compound money like column one: A Roth IRA. It's such a good vehicle that it is truly amazing that the government hasn't gotten rid of it.

The way a Roth works is that you earn money, you pay tax on the money you earned, and you then can invest up to about $6500-$7500 a year in a Roth IRA. That money has already been taxed, so they aren't going to tax it again. The special quality of the Roth is that the money you make on the money you put in is never taxed. Ever. EVER!

And even better, you can invest a Roth in almost anything. Peter Thiel, a founder of Paypal, bought 1.7 million shares of PayPal for $0.001 per share. $1700. That turned into $30 million when eBay bought out PayPal for $19 a share in 2002. With that $30 million to work with in the Roth, Peter bought into Facebook, Yelp, and Palantir, and by 2019 his little ol' Roth had over $5 billion in it. The gains are all tax-free. God bless him. Of course, he can't take the money out until he turns 59 and a half but considering that Thiel has billions outside the Roth, you shouldn't worry about his financial well-being.

SIMPLE IRA

This vehicle, the Investment Retirement Account or IRA, receives money before you pay taxes on it. It is known as a Qualified Account, government gibberish, which means it is approved for pre-tax money.

The obvious advantage of an IRA is that you can put money in that you would have paid to the government. Let's say you could put away $4000 a year after taxes are paid. If you put $6000 a year into an IRA, it would feel the same to your bank account because the extra $2000 is money you would have paid in taxes.

You can invest an IRA in almost anything, like the Roth, but unlike the Roth, when you start taking money out after you retire, you'll pay taxes on all of it as it comes out. And you'll be forced to start taking it out and paying taxes on it at age 70 and a half.

That said, it's still a really good deal. If you're not sure about that, just refer to the chart above. Your IRA can produce the results in column one. Not using an IRA gets you the results in column two.

$4 million is better than $2 million, yes? But, of course, because it is such a good deal, the government limits how much you can put in each year to that same Roth amount of $6500-$7500, depending on your age.

SEP IRA

A SEP-IRA is just a regular IRA, except it's only available to small businesses and, man, it lets you load up the truck with pre-tax money. If you run a small business, you can open up a SEP-IRA where you can put away, pre-tax, up to 25% of your compensation to a max of $66,000.

Yeah, you read that right. Of course, that means you're doing alright - making about $260,000 a year. Go for it if your business qualifies.

CASH BALANCE PLAN (AKA DEFINED BENEFIT PLAN)

This is the grand poo-bah of retirement plans for those who didn't put much away while building a nice business. This plan is the jackpot for a Sub-S corporation that is distributing some serious cash to the owners or a medical practice group doing the same thing - throwing off cash after years of struggle.

The Cash Balance Plan (they are clearly trying to hide the massive benefit of this plan behind a completely innocuous name) provides a defined benefit in the form, theoretically, of an annuity that the plan will buy when you retire. The annuity's size depends on how much you make every year and how little you put away toward retirement.

If you're suddenly making a load of money and are getting up there in years, this plan can put away hundreds of thousands of dollars every year until that theoretical annuity is funded. Some people have parked over $1 million away tax-free in one year.

If you qualify for this plan, you're doing well and probably have some pro advice coming at you. But if they've never mentioned the benefits of a cash balance plan, you might want to poke at them with a sharp stick and get them looking into it.

401K

And here's the most common plan - the 401(k). 401(k) 's are qualified plans offered by your employer. They have pretty much replaced the old Defined Benefit Plan that my dad had.

Those defined benefit plans gave employees a defined amount of money monthly upon retirement for life. Employers don't like them because they are on the hook to invest the employees' retirement accounts successfully enough to pay the lifetime benefits. Employees didn't like these accounts because the benefits were small compared to putting money in the stock market via an IRA.

One of the major benefits of a 401(k) is that your employer may offer a matching program where they will match whatever you put in up to some amount. That's awesome. If your employer offers a 401K matching program, you should take advantage of this opportunity to double your money for free.

401(k)s don't offer the same level of investment control as an IRA since they are structured by the employer you work for. In many cases, these restrictions are put in place because companies are fearful of employees having too much control.

Given how litigious America has become, there is reasonable suspicion in the head office that employees who are free to invest in anything might lose everything and then sue the company for giving them the freedom to do so. Hey, if you can make millions for spilling coffee in your own lap, why not sue those bastards for treating you like an adult? They should know you're an idiot, right? Not only that but an idiot unwilling to take responsibility for his actions. Get the right bunch of idiot jurors, and you could score big. So they restrict your investments in most 401(k) programs.

However, they don't have to. You could invest in a 401(k) just like an IRA if your company lets you. The way to get them to let you is to send them a letter expressing your desire to be treated like an adult. But also let them know that by restricting you to a limited number of investment choices, they may not be complying with their fiduciary responsibility. Give it a shot. They can only fire you.

Once you leave this employer (see above), you can (and should) roll your 401(k) over into an IRA. Any online broker will be happy to show you how simple that is. Just give them a call.

HEALTH SAVINGS ACCOUNT (HSA)

Funds set aside in a health savings account (HSA) can be contributed toward any medical expenses that a person may be responsible for.

The benefit of an HSA is that you get another vehicle to put in investment capital pre-tax. You can put in $3650 per year, and your contributions to this account are tax-deductible, returns are not taxed until withdrawal, and you won't be taxed on withdrawals for qualified medical expenses. The last part of the previous sentence is important. If you choose to spend these funds on expenses that are not medically related, you will be fined.

However, if you never get sick or hurt, the contributions and your compounded return on those contributions will add up year by year tax-free until you decide to start withdrawing the money, at which time you get taxed. That means the HSA account is a vehicle just like an IRA, except it can be used to cover medical expenses.

Picking the Investment Vehicle for You

Choosing an investment vehicle is simple. Fill up an HSA, so you're medical is covered. Then load a ROTH for maximum long-term gains. Add in a SEP-IRA in your business to save even more money pre-tax. And finally, if you're of an age and making bank, get a Cash Balance Plan going.

Once you have the vehicle, the fun part starts - picking an investment to put in that vehicle. Here's where the rubber meets the road because not knowing how to invest stops most people from taking advantage of these vehicles.

When it comes to investing for your retirement, ignorance is not bliss. To ensure that you're always making the right investment choices, knowing how to invest is crucial. Fortunately for all of us, learning how to invest is actually much simpler than it is made out to be.

That's why I have my Complete Guide to Investing for Beginners, so you know exactly what choices to make when choosing your investments. Click the link for a free copy and get your vehicle's motor running to take you to financial independence.

How to Pick Rule #1 Stocks

5 simple steps to find, evaluate, and invest in wonderful companies.