When I first started investing, I was working as a Grand Canyon river guide making $4,000 a year. That's not a typo. I lived out of a tent and everything I owned fit in a duffle bag. So when I tell you that the amount of money you start with is not what determines your success as an investor, I mean it from personal experience.

When it comes to money, "small" means something different to everyone, so I'll walk you through a few small investment ideas based on your budget.

Most people hold off on investing because they think they need more money before they can start. I hear it all the time. The truth is, the amount you start with matters far less than the strategy you bring to it. Whether you have $20 or $1,000, the same Rule #1 principle applies: don't lose money. That single idea changes how you think about every investment decision you will ever make.

With the right strategy, starting small can be an advantage rather than a shackle. Over time, even small investments can grow into something significant. Read on for how to invest in stocks for beginners with little money.

A Strategy for Making Small Investments

Before we dive into specific small investment ideas, it helps to understand what investing actually is and how to get the greatest return on your money.

Whether you're investing with small money or big money, you will follow the same basic investing strategy. The best way to invest $1,000, $500, or even $20 is the best way to invest $10,000. Investing is always investing.

The value of what you're buying is always the first question. What is this business actually worth? What is the price today? If the price is less than the value, you're off to a good start. That gap between price and value is where real investing begins.

What's your Investing IQ?

See how you stack up against other investors.Determine the Best Type of Small Investment for You

If you are just getting started, it is worth knowing that some people use high-yield savings accounts or certificates of deposit as a first step, especially while building an emergency fund. These are low-risk options that can help you protect cash in the short term. But if your goal is to build real, lasting wealth over time, they are a starting point, not a strategy. There are 15 types of investments worth understanding before you decide where to focus.

There are lots of different types of investments you can make, but not all investments are great for small amounts of money. For example, you can't invest in real estate with $500, and even though you can invest $500 in Exchange Traded Funds and bonds, it doesn't mean you should.

If you put $500 in ETFs or mutual funds each year for the next 30 years and get the long-term historical return of 7%, all you'll have in 30 years is $45,000 (less fees for mutual funds).

Take bonds next. With a historical return of 5% over the next 30 years, your investment will grow to around $33,000. Bonds may be the safest way to invest, but how safe is a retirement of $33,000?

The answer is stocks. When you learn to invest the Rule #1 way, stocks are where your money can do its most meaningful work over time.

Later, I'll show you how to calculate how much you can have in 30 years if you invest $500 in the stock market. Hint: it's a lot more than the other options.

Overcome Your Fear of Investing in the Stock Market

The stock market can feel scary and risky if you don't know what you're doing. But one of the core principles of Rule #1 investing is to only invest in businesses you understand. When you understand what you own, the fear starts to dissolve.

Putting money into things you don't understand is not investing. It's speculation. And speculating on stocks is no different from gambling.

Frankly, that’s the way most retirement accounts are managed. The account managers are speculating on someone being willing to pay more for a stock tomorrow than you paid today.

This is likely to be true in the long run, but you have to ask yourself, “How long is the long run?” and “How much more will you make?”

That’s why you should consider learning how to invest (real investing, not speculation). Real investing is buying wonderful businesses you understand at prices that make sense. When you do that, you are not guessing. You are making a reasoned decision based on value.

Bottom Line: "Risk comes from not knowing what you are doing." — Warren Buffett

Understand How Small Investments Pay Off in the Long Run

The most important move you can make is a simple one: start. It is better to begin with a small investment now and add to it over time than to wait and lose out on the returns and the compounding growth you could have had.

Every day you don't invest, you are losing out on compound interest. With compound interest, when your money grows, its growth is also invested.

There is a tool I like to use called the Rule of 72 that explains the power of compounding interest and shows you just how fast your money can double. This is how even small investments can grow into something significant over time.

What Do I Actually Want From This Investment?

If you want to make money fast, go to Las Vegas, bet everything on black, and hope for the best. That is gambling, not investing. The two are not the same thing.

I don't gamble with money. I buy wonderful companies at attractive prices and I hold them for the long term.

If you really want to learn how to invest, it takes due diligence and patience. But the long-term payoff is worth it. Warren Buffett started with a small amount of money too. What he had was not capital. It was knowledge.

That is good news if all you have right now is a small amount. There are no real barriers to building wealth if you are willing to learn how to do it properly. When you know how to evaluate a business the way the world's best investors do, you are not taking wild risks. You are making informed decisions.

So, what are the best small investment ideas for $1,000, $500, or $20? Let's break it down.

How to Invest $1,000

Let's get specific with small investment ideas for $1,000. Even if you don't have $1,000 to invest yet, these strategies will help you understand how to invest with little money at any amount. The principles are the same regardless of where you are starting.

Make a Promise to Yourself

You have a small amount of money to invest, but are you really ready to put your money where your mouth is?

If so, make a promise to yourself that you are going to do your due diligence to find the right companies, buy them at attractive prices, and double your $1,000 over the next 5 years.

Once you have made that commitment, you are ready to move on to the next step.

Research the Company — The Four M's

The key thing to understand is that I make money by buying wonderful companies and buying them on sale. So what makes a wonderful company?

Charlie Munger, partner of Warren Buffett, said there are four things you've got to focus on when you invest your $1,000, or any amount of money, in a company:

Number one, be sure you're capable of understanding the business that you're getting into. Number two, be sure that this business has this thing that we call a moat: something deeply embedded in it that protects it from the competition. Number three, make sure that the management team is made up of people who share your values, have integrity, and are talented.

And finally, make sure you buy it on sale. "Sale" means at a purchase price with a margin of safety.

I call these the four Ms. Here's what each one looks like in practice.

Meaning: Only invest in businesses you genuinely understand and would be proud to own. If you can't explain what the company does and why it makes money, it's not the right fit for you.

Moat: Look for a durable competitive advantage that keeps rivals out. That might be a powerful brand, a cost structure competitors can't match, or a product customers simply can't replace.

Management: Study the people running the business. Are they honest? Do they think like owners? Do their actions line up with their words?

Margin of Safety: This is how you make sure you're not overpaying. You figure out what the business is actually worth, its Sticker Price, and then you only buy it when the market is offering it at a significant discount. That gap between price and value is your protection. To learn how to walk through this process step by step, start with this beginner's guide to investing in stocks.

Avoid the Temptation to Diversify

Contrary to popular belief, you don't need to diversify when you invest in a few wonderful companies that meet the criteria above. Diversification is what speculators use to safeguard uncertain stock picks.

Once you know how to evaluate a business the Rule #1 way, you won't need to spread your money thin across dozens of funds hoping some of them work out. A few wonderful companies bought at attractive prices will serve you far better than a broadly diversified portfolio built on guesswork.

Stick to a few wonderful companies and you'll be better off.

How to Invest $500

You may be thinking, "$1,000 is a lot of money. What about $500?" If you're asking yourself that, remember: the best way to invest $500 is the best way to invest $1,000 is the best way to invest $10,000.

It's not the amount of money that makes a great investment. It's the strategy.

The Strategy Is the Same — The Opportunity Is Real

Starting with $500 is not a limitation. It's a starting point. And starting points have one thing going for them that nothing else can give you: time.

The earlier you start, the harder compound interest works in your favor. Waiting just 10 years means you would need to invest roughly four times as much money to end up in the same place. Time is the one advantage no amount of money can replace.

Rule #1 investing is not about taking on more risk because you have less to lose. It's about taking on less risk because you know exactly what you own. The Four M's work just as well with $500 as they do with $500,000. Find a wonderful business. Make sure it has a moat. Evaluate the management. Buy it at a Margin of Safety price. That's the whole game, regardless of how much you're starting with.

Utilize the Magic of Compound Interest

If you can continue to invest $500 per year the Rule #1 way, you can watch your initial investment grow even more.

It's the power of compounding interest that can make you rich even with little money.

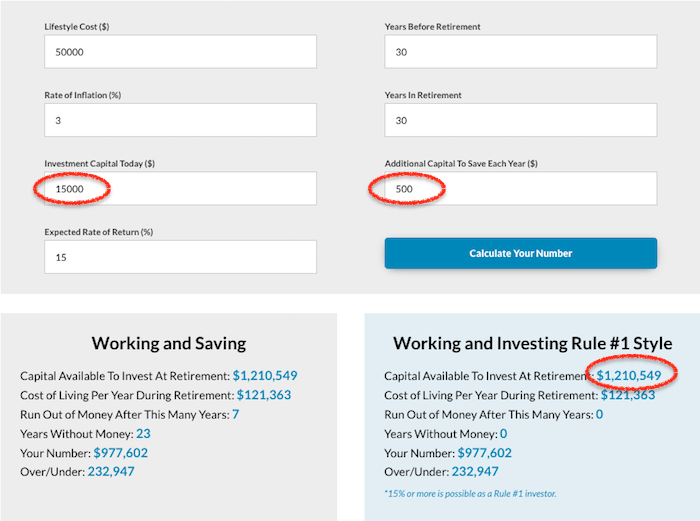

Let's take a look at this example: If you started out with $15,000 saved and contributed an additional $500 per year for 30 years, you could end up with $1.2 million when you're ready to retire. See how I calculated this using my free Retirement Time Calculator below.

Plug in your own values using how much you have to invest today and how much you can contribute to your portfolio each year to calculate how much you could have for retirement.

(This screenshot from my free retirement calculator shows how much you'd have if you invested $500 using Rule #1)

Want a quick way to feel this in your bones? Use the Rule of 72. Divide 72 by your expected annual return and you get the number of years it takes your money to double. At a 15% annual return, your money doubles about every 5 years. That means $500 today becomes $1,000 in 5 years, $2,000 in 10, $4,000 in 15, and so on, without adding another dollar. Now imagine what happens when you keep adding $500 every year on top of that.

Once you're ready to move from understanding the framework to finding an actual company to invest in, the Rule One Calculators are where to start. The Sticker Price Calculator will show you what a business is actually worth so you can spot a Margin of Safety price when Mr. Market offers one.

How to Invest $20

Maybe your idea of a small investment is closer to the $20 range. That's totally fine. Baby steps are better than no progress at all.

The fact that you're even thinking about investing when you only have $20 means you're in the right mindset. One of the best things you can do to begin investing when you have very little money is to form good habits. Practice these good habits with $20 and you'll have a rich future ahead of you.

The Value Investing Cheat Sheet

Learn what 10 steps you should take to make smarter investing decisions

Don't Wait

You can start forming good habits by taking money out to invest as soon as you receive your paycheck.

Most often, people end up taking the exact opposite approach, waiting to see how much money they have left over before they invest. If you wait to see how much money you have left over before investing it, the number will almost always be a big 'ol zero.

Instead, invest your $20 straight out of your paycheck and watch it work for you. Setting aside money to invest right away, even as little as $20, can become a natural, nearly subconscious act when you do it regularly.

Don't Save It

Saving isn't inherently bad, but if you want to get a great return on your money and create generational wealth, it won't happen by saving it.

Most savings accounts offer interest rates that struggle to keep pace with inflation. That means the money sitting in your savings account is not really growing. It's slowly losing purchasing power over time. Your dollars today will buy less tomorrow if all they do is sit.

Think of your investment account as your saving account and you'll be well on your way to "saving" $10,000 this year.

Avoid Money Traps

It's simply too easy to spend money rather than invest it if you make spending it an option. Things like fancy cars, big houses, and weekend nights out can mean you have less to invest. Avoid these money traps and focus on the promise you made to yourself. Take your $20 and invest it in a great company rather than its fancy product.

Use It as a Stepping Stone

No investment is too small. Small investments such as $20 still grow, especially when you invest $20 on a regular schedule. That's really all it takes. Not only will your $20 investment grow, but it will also help you conquer your fear and keep your promise to yourself.

How to Invest With Little Money or No Money

Anyone can start investing, no matter how little they have right now. I know this firsthand.

When I first learned to invest, I was working as a Grand Canyon river guide making a whopping $4,000 a year, that's not a typo. I lived out of a tent and all of my belongings could fit into a small duffle bag. I know what it's like to try and invest when the price of a single share in many companies is more than you have to spend.

I am living and breathing PROOF that investing is something anyone can succeed at with the right approach, no matter how much or how little money they are starting with.

What you do have is a starting point. And a starting point, paired with the right framework, is all you need. Everyone starts from somewhere. There is no such thing as having too little to invest.

Benefits of Investing With Little Money

There are real advantages to starting with small amounts of money. Here is what they look like in practice.

You Are Starting Sooner

Investing when you have little money means you are starting sooner rather than later. When you start now, even small amounts of money put into the market can grow into legitimate sums of money as the years go by.

You Have Less to Lose

Another advantage of investing with little money is that there is less to lose. While it may sound like a lot of money and be painful at the moment, losing $500 is not going to dramatically change your life the way losing a fortune would. Small investments help you get comfortable with the ebbs and flows of the market and take small losses in stride.

You Can Learn the Ropes

If you don't have much money to invest, you really need to wait for Rule #1 events that cause great companies to go on sale. It makes even more sense to seek out great deals on companies because great deals are all you can afford. When you learn the skills to make great decisions on small investment ideas, you can apply them to big investment ideas later on.

Continue to Learn More Small Investment Strategies

Investing isn't about just jumping in with $1,000 and it's not about waiting until you have more to jump in with. It's about finding wonderful businesses you want to own and finding the right time to buy them.

Whether you have $1,000, $500, or $20, the strategy is the same. Find a wonderful business. Evaluate it through the Four M's. Buy it at a Margin of Safety price. And let compound interest do the rest. That is not a complicated idea. But it is a powerful one, and it takes practice to apply well.

If you want to go deeper on low-risk investments or explore what growing your portfolio looks like at the next level, the best way to invest $1,000 and the best way to invest $10,000 are good places to continue from here.

The best next step is to take what you have learned here and put it into practice with real coaching. At the Virtual Investing Workshop, I walk through the Rule #1 framework with you and my team of live coaches over three days. You will learn how to research companies, apply the Four M's, calculate a Sticker Price, and identify when a wonderful business is available at a Margin of Safety price. All from the comfort of your home.

Attend a Rule #1 Workshop

Learn how to conduct research, choose the right companies for you, and determine the best time to buy.