Understanding the Raising Interest Rates: Key Trends and Insights

We've all felt it. Grocery prices that keep creeping up, housing costs that just won't budge, and energy bills that seem to surprise us every month. Even as we enter a new year, the annual inflation rate continues to shape the US economy. Ultimately, it affects the financial decisions we make about spending money.

But what's really raising interest rates? And why, after so many moves from government agencies, hasn't it fully cooled? We'll examine what’s happening now while taking in lessons from the past. Put those together, and we can position ourselves as smart investors, even when prices rise.

Let's break each topic down together.

Inflation-Ready Checklist

Learn what to do with your money during inflationary times

What is Inflation?

Let's start with the basics.

Inflation is basically when your money doesn’t stretch as far as it used to. That’s because the purchasing power of the dollar drops over time. This means you need more dollars to buy the same goods and services. The most common way to track this is the Consumer Price Index (CPI). This measures the average price changes across a broad range of consumer goods and services.

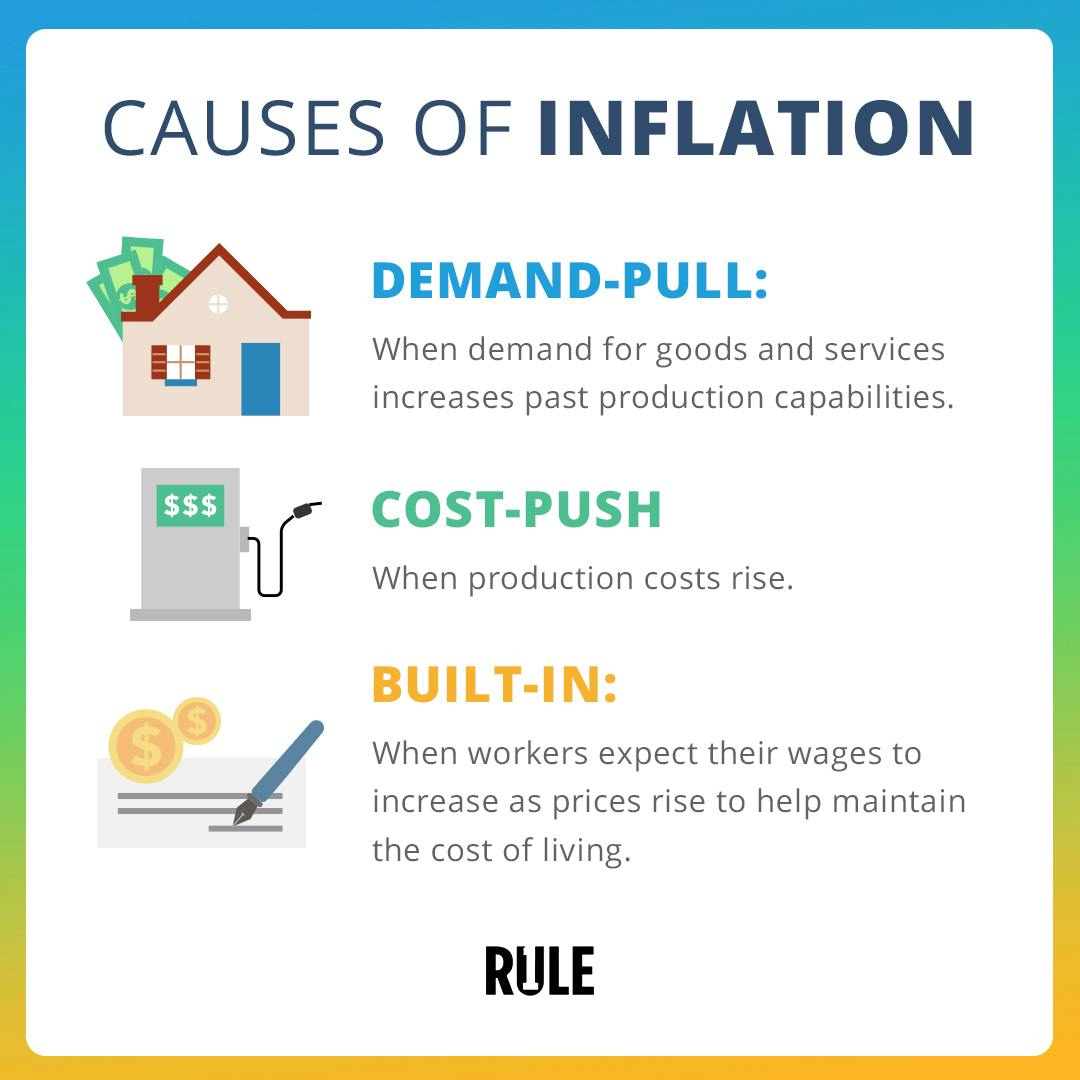

But here’s where it gets interesting: not all inflation is created equal. Economists talk about three main types:

Demand-pull inflation:

Imagine everyone suddenly wants to buy new cars, but there aren’t enough to go around. When demand outpaces supply, prices tend to rise. This happened big-time after the pandemic. Consumer demand surged thanks to stimulus checks and pent-up spending.

Cost-push inflation:

This is when production costs go up due to rising taxes or increased prices for raw materials or energy. Businesses then pass those higher costs on to the consumer. Think about how food prices and energy prices spiked when supply chains got tangled or when natural disasters hit.

Built-in inflation:

Sometimes, just the expectation that prices will keep rising can lead workers to demand higher wages, which in turn causes businesses to increase prices. It’s a bit of a feedback loop, one that can keep inflation stubbornly high.

All these terms can sound like economist-speak. But at the end of the day, it's about how much your money can buy. Lately, as inflation rises, every dollar you make buys less.

What Causes Inflation?

You might be wondering, “Didn’t the Federal Reserve raise interest rates a bunch of times to combat inflation?” Yep, they sure did. In fact, the central bank’s monetary policy has been front and center since 2022. The interest rates back then were at levels we haven’t seen in decades.

So, what gives? Why are we still seeing inflation above the Fed’s 2% target?

Let's look back for a second. During the COVID-19 pandemic, the US government rolled out massive stimulus packages to keep the economy afloat. While this was necessary, it also led to a surge in the money supply and, ultimately, higher inflation.

Core inflation reflects the long-term, underlying trend in price changes. It is shaped by economic forces that influence persistent inflationary pressure over time:

Wage growth

Monetary policy decisions

Overall demand in the economy

Energy Prices, Goods, and Services

Prices of goods and services such as energy tend to be more volatile. For example, clothing and apparel prices would be affected by a mix of supply-side and demand-side factors.

On the supply side, production costs, input availability, and global supply chain conditions influence how expensive goods become. On the demand side, consumer spending patterns, income levels, and purchasing confidence shape how strongly people compete for available products and services. Together, these factors directly impact how prices move across the broader economy.

Labor Market and Wage Dynamics

Today's labor market remains surprisingly resilient. Unemployment remains low, though wage increases have slowed from the hot pace of 2022–2023, with real average hourly earnings at just over 1% from 2024-2025. In 2026, the global unemployment rate is projected to remain stable at approximately 4.9% as per International Labour Organization. While that's helped moderate some price pressures, strong consumer demand has kept upward pressure on essentials, like housing, food, and services.

For retirees and those near retirement, this inflationary environment poses serious challenges. At just 3% annual inflation, the cost of living nearly doubles over 25 years. If, as some predict, inflation averages closer to 4–5%, the retirement savings needed to maintain your lifestyle could balloon to five or six million dollars for many households. This is up from the two million often cited a few years ago.

Housing Market: A Stubborn Source of Inflation

Housing remains one of the most persistent drivers of inflation. While home price growth has slowed, affordability remains a crisis. Mortgage rates, even after moderating, are still well above their pre-2022 levels: hovering near the 6% mark at the end of January 2026, which prices out many first-time buyers. In fact, higher mortgage rates significantly decrease purchasing power; a 1% rate increase can reduce a buyer's budget by up to 10%. That’s a huge difference when you’re house-hunting.

Tight inventory continues to fuel inflation and bidding wars on entry-level homes. And let’s not forget: higher interest rates on mortgages, car loans, and credit cards reduce disposable income for other purchases. When more of your paycheck goes to debt payments, there’s less left over for everything else.

Inflation Expectations and the Inflation Reduction Act

The Federal Reserve Bank continues to project that inflation will remain elevated above its 2% target for years to come. This is despite aggressive monetary policy and interest rate hikes that have helped cool some price pressures. The Inflation Reduction Act, passed in 2022, laid the groundwork for long-term clean energy investments. Unfortunately, its immediate effect on consumer prices has been modest.

Importantly, investor Ray Dalio has shifted his recent warnings away from specific inflation rate forecasts and toward the broader structural risks facing the U.S. economy. Dalio, along with several senior economists, has expressed deep concern about the nation's mounting debt burden. He warned that without meaningful policy reforms, the U.S. could face a debt crisis. This can then lead to higher interest rates, economic instability, and potentially renewed inflationary pressures

For investors, this underscores the critical need to build resilient, inflation-aware portfolios. It's no longer just about watching inflation numbers. It's about understanding the economic risks that can ripple through markets and affect retirement planning, wealth-building, and investment strategy.

The Numbers: Inflation Rate and Key Indicators in 2026

So where do we stand now? Here’s what’s happening in 2026:

Inflation Rate: The annual inflation rate is hovering around 4% by the end of 2026, down from the 9% peaks of 2022, but still above the Federal Reserve’s target.

Core Inflation: When you strip out volatile food and energy prices, core inflation is still running above 2.2%, reflecting broad-based price increases.

Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE): Both are showing a percentage change that’s higher than historical averages. This is driven by a broad range of categories from housing to medical care.

Unemployment Rate: Remains low, supporting strong consumer demand and contributing to rising wages.

GDP Deflator and Gross Domestic Product: The GDP deflator, a measure of price changes across the economy, confirms that inflation is impacting a wide range of goods and services.

It’s a complicated picture, but the message is clear: high inflation isn’t just about one thing. It’s a combination of factors that keeps upward pressure on prices.

Inflation-Ready Checklist

Learn what to do with your money during inflationary times

Major Events That Shaped The Current Inflation Rate

A little history helps explain where we are now:

COVID-19 pandemic (2020–2021): Global supply chain issues, reduced production, and unprecedented government spending set the stage for high inflation.

Federal Reserve's response (2022–2024): The central bank raised nominal interest rates to levels we hadn't seen in decades. This cooled demand but didn't eliminate inflation.

Inflation Reduction Act (2022): This was the government's largest investment in climate and energy, aiming to lower long-term costs. Its near-term impact on consumer prices, though, has been modest.

We've also seen labor shortages and global financial crises play a part in the past years. It's a perfect storm of economic data points all hitting at once.

Historical Data and Parallels

History gives us important context.

World War II and the Korean War saw demand-pull inflation as economies boomed and supplies ran short.

The 1970s were marked by cost-push inflation, where oil shocks and wage-price spirals drove prices higher.

The Iraq and Gulf Wars also saw oil price spikes, hitting consumers and businesses hard.

The 2008 housing crash reminds us how financial excess and loose lending can collapse the market. It's a cautionary tale that still influences housing policy today.

The early 2020s saw high inflationary pressures drive up costs for consumer goods, particularly food and energy.

What's different now is the combination of these pressures. Political concerns, such as a government shutdown, can also indirectly affect the overall inflation rate.

How Does High Inflation Impact Your Everyday Life?

Let’s get real for a moment. High inflation isn’t just an abstract economic term. It’s something we all feel. You might be budgeting for the rising prices of groceries, trying to save money for a house, or planning for retirement.

Here are some common questions we hear all the time:

“Is my emergency fund enough?”

When prices rise, your emergency fund might not stretch as far. It’s a good idea to review your savings and consider high-yield savings accounts to help your money keep pace with inflation.

“Should I buy a house now, or wait?”

The housing market remains tight, and fixed-rate mortgages are pricier than before. If you’re thinking about buying, factor in not just current prices. Think about where interest rates and housing expenses might head.

“How can I protect my investments?”

In an inflationary environment, traditional diversification might not be enough. Focus on wonderful businesses with pricing power. Opt for commodities that benefit from higher costs. Keep learning about how to assess value.

And if you’re nearing retirement, remember: even 3% inflation can double your cost of living over 25 years. Planning ahead is more important than ever.

How to Invest During Inflation

Inflation is a challenge in the modern economy, but it's one you can navigate if you pay attention to new data. And here's where the Rule #1 philosophy comes in.

Our message is clear: diversification alone won't protect you. Instead, focus on:

Revisiting Your Portfolio: Don’t just diversify. Choose investments that can thrive in an inflationary environment.

Staying Liquid and Flexible: Keep some assets in high-yield savings accounts or other liquid vehicles.

Wonderful businesses: Companies with durable competitive advantages (moats), pricing power, and strong cash flow.

Commodities and sectors that benefit from inflation: Think energy, agriculture, and select industrials.

Your own education: Learn how to assess companies, read financial statements, and understand valuations.

And don't forget to grab the Inflation-Ready Checklist to ensure your portfolio is built to last.

Final Takeaway on Raising Interest Rates

While inflation has moderated from its peak, it's not going away anytime soon.

The key for investors is to adapt: focus on businesses that can thrive in this environment. Stay informed of every monthly increase and observe the performance of the businesses you invest in. Did they do well in the previous month? How about the previous year? Build a portfolio designed to preserve and grow your wealth over the long term.

Remember, economic growth isn't always smooth, and price stability is never guaranteed. Global events may cause an increased demand for goods, and efforts to control inflation may not succeed. But with the right mindset and a solid investment strategy, you can weather the ups and downs of inflation.

Curious about the latest economic data? Want to stay ahead of price changes? Or, maybe you just need help navigating higher prices. Whatever it is, keep following our blog for more updates. Together, we can make sense of the numbers and make smart decisions for our financial future.

Attend a Rule #1 Workshop

Learn how to conduct research, choose the right companies for you, and determine the best time to buy.

**Editor's Note (Updated 2026): This article was originally published in 2025 and has been significantly updated in 2026 to reflect current examples and Rule #1 investing insights.