Every once in a while a student submits a perfect homework. Here's one, with my comments at the very bottom. This is a good opportunity to learn by example.

Dear Phil Town,

As they say, Wisdom begins in wonder. I came across your blog by accident, started reading with a lot of cynicism, and now have incredible respect and trust in your advice. I am a 28 year old software engineer in Phoenix and have 50k in savings which I hope to invest wisely over the next six months. Here is my first homework. [Infosys -- INFY]

Meaning

Infosys is a global technology services company based out of India. It is in pretty much the same business as Cognizant Technology Solutions (CTSH) except that INFY is the top dog in this market. Infosys has over 49,422 employees and its corporate headquarters is in India.

Infosys’s Vision:

"To be a globally respected corporation that provides best-of-breed business solutions, leveraging technology, delivered by best-in-class people."

I know people who work at Infosys and am amazed by the speed with which they are hiring -- In 2000, they had 10,000 employees, in five years they have made it five times as large.

I would definitely buy this business if I could especially because this is a growing business in a growing industry with a good management team and a good moat.

Moat

I looked at Sales, EPS, ROI, ROE, Equity, Cash, Debt. [Click on chart to view larger.]

In 2001, they seem to have had exploding growth -- maybe due to the aftermath of the Y2K problem; if we exclude that anomalous growth and look at the rest of the years, they have had stable and high growth in all numbers. The only red mark is the FreeCashFlow/Share number for 2005.

Given above, they definitely have a Moat and they seem to be widening and deepening the moat. As you pointed out in the post for CTSH, outsourcing is an industry based on relationships- companies are doing heart surgery when they send work overseas, and Infosys seems to have built a brand moat around it.

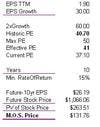

MOS

The analysts are predicting 31% growth. Bvps grew at 29% last year. My most conservative guess is 30%. I had to prune some very good numbers from the historic P/E ratios too since they seems to have had amazing growths during 99-2001. So I culled the P/E of 172, 411 and 136 and came up with a historic P/E of 40 based on the last four years.

[Click on chart to view larger.]

Infosys is currently trading at $74.73

Management

N. R. Narayana Murthy used to be the head honcho at Infosys- He was definitely a Level 5 leader and has cultivated a posse of leaders to take over the mantle when he leaves. Nandan M. Nilekani is now the CEO and has been pivotal in enabling the growth of not only Infosys but the outsourcing industry in India.

Kevin did a great job. Here's what I told him:

Hi Kevin,

I really like your work on INFY. They are the big dog in the outsource IT market and you already know I like that area. And I like INFY a lot. It's on my watch list, too. Like Cognizant, the CEO is an Indian hero, and is by all accounts great to work for. The issues raised about CTSH moat apply equally to INFY so we have to watch the arrows and pay a lot of attention to the big guys -- because if problems occur, we'll see it in institutional pull-out first and hear about it when it's too late. That said, if these guys can keep this growth up, we're going to rack up some very sizable returns on their labors over the next ten years.

I have no, as in zero, criticism of your work. Its a solid Rule #1 analysis. Nice job. You catch on fast.

Now go play!